Unveiling the Core Tax-Saving Tools Behind the Rockefeller Family’s Wealth Legacy — Life Insurance

Throughout the history of wealth preservation, the Rockefeller family has not only been renowned for the longevity of its fortune but also for pioneering a sophisticated wealth management model — the “family office.” This family-centered structure integrates tax planning, trusts, investments, and insurance into a comprehensive system that has since become a blueprint for countless ultra–high-net-worth families.

In this article, U.S. tax attorney Yiyan Cao provides an in-depth explanation of one of the most critical components of that system: the role of life insurance within the U.S. tax framework. A deeper discussion of how family offices further enhance tax efficiency and asset protection will be explored in future articles.

The Fundamental Role of Life Insurance: More Than Protection, a Tax Tool

When people think of life insurance, they often view it simply as a financial safety net for loved ones. Under U.S. tax law, however, life insurance serves a much more powerful function: death benefits are generally exempt from income tax. This treatment stems from Section 7702 of the Internal Revenue Code (IRC), which defines what qualifies as a life insurance contract. If a policy meets these statutory requirements, beneficiaries may receive death benefits free of income tax.

China’s Individual Income Tax Law contains similar principles.

That said, life insurance is not entirely tax-free. For wealthy families, estate tax remains a significant concern. If the insured owns the policy or retains certain ownership rights—such as the ability to change beneficiaries or borrow against the policy—the full death benefit may be included in the taxable estate. This could subject the proceeds to federal estate tax at rates as high as 40%. Notably, the federal estate tax exemption is scheduled to be $15 million in 2026 (for individuals under U.S. tax law).

A common solution is to hold the policy in an Irrevocable Life Insurance Trust (ILIT). When the trust owns the policy, the insured no longer holds incidents of ownership, and the death benefit is excluded from the taxable estate.

The Billionaire Strategy: Private Placement Life Insurance (PPLI)

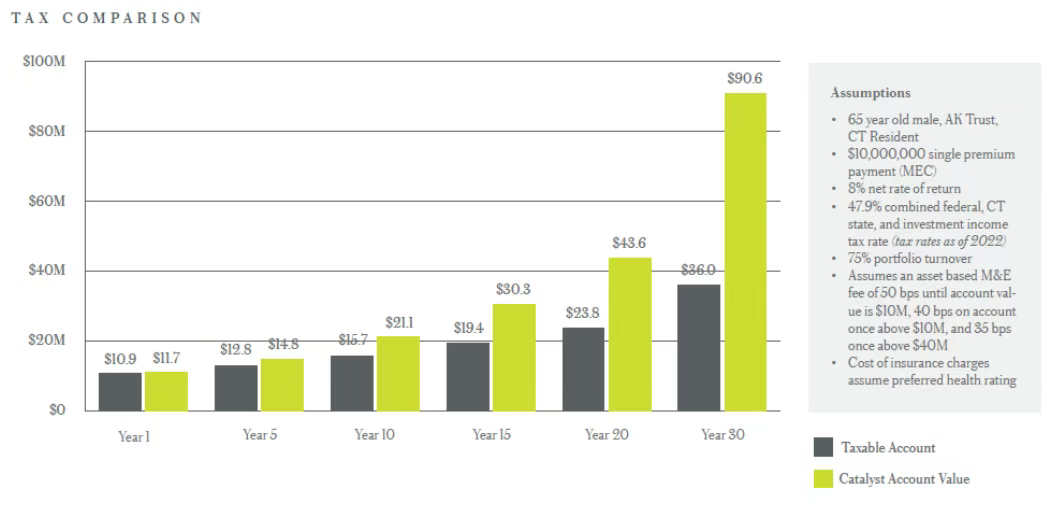

At the very top of the wealth pyramid, ultra-high-net-worth individuals often use an advanced planning tool known as Private Placement Life Insurance (PPLI). PPLI still qualifies as a life insurance contract under U.S. tax law, but unlike retail policies that limit investment options to mutual funds or fixed-income products, PPLI allows high-net-worth policyholders to customize the underlying investments.

Through PPLI, investors may place hedge funds, private equity, or other alternative investments—often assets that would otherwise be subject to high tax burdens—inside the insurance structure. Hedge funds, for example, may face combined federal and state taxes approaching 50%.

These investments can grow on a tax-deferred basis, and upon the insured’s death, the death benefit is paid out income-tax free. When held inside an ILIT, estate taxes can also be avoided. In our legal practice, we have observed that many poorly structured insurance trusts fail under scrutiny, particularly when challenged by the IRS or creditors.

The IRS has long monitored the use of PPLI and has made clear that policyholders cannot directly control investment decisions. When properly structured, however, PPLI remains one of the most powerful wealth preservation tools available to ultra-high-net-worth families.

Political Storm Triggered by PPLI: A $40 Billion Wealth Tool Under Senate Scrutiny

Because of its powerful tax advantages, PPLI has drawn significant political attention in Washington. In early 2024, the office of Senator Ron Wyden, Chair of the Senate Finance Committee, released a report alleging that PPLI has been used by ultra-wealthy individuals as a large-scale tax avoidance tool.

The report noted:

Approximately $40 billion in PPLI assets are held by only a few thousand wealthy families;

These policies are marketed as “insurance wrappers” for hedge funds and private equity investments, enabling avoidance of income, gift, and estate taxes;

Lawmakers called for stronger regulation to close what they viewed as a tax loophole for the wealthy.

In response, Senator Wyden introduced draft legislation proposing expanded reporting requirements, stricter ownership rules, and limitations on tax benefits. However, the proposal failed to gain sufficient bipartisan support. The reason is clear: PPLI sits at the intersection of powerful insurance companies, private equity firms, and family offices, all of which exert significant influence in Washington.

In short, while regulators attempted to tighten the reins, market forces prevailed. As long as PPLI structures comply with IRC Section 7702, they remain legally protected under current law.

Compliance Warning: What the Webber Case Teaches Us About Crossing the Line

Although PPLI is a legitimate planning tool, compliance is critical. If the policyholder directly or indirectly controls investment decisions, the structure may violate the “Investor Control Rule,” causing the policy to lose its tax-advantaged status.

The landmark case Webber v. Commissioner (144 T.C. 324, 2015) illustrates this risk. Mr. Webber established a PPLI policy and directed investments into companies in which he served as a director. He not only held ownership interests but actively controlled investment decisions. The U.S. Tax Court ruled that the insurance company acted merely as a passive conduit, and the investments were effectively owned by the taxpayer.

As a result, the policy lost its tax protection, and all gains were taxed directly to the policyholder, along with penalties. This case serves as a clear warning: once the policyholder crosses the line of control, PPLI loses its tax advantages.

To remain compliant, policyholders must ensure that:

They do not participate in investment decision-making;

Investment selection is made by independent managers or insurers;

No control, board participation, or related-party transactions exist between the policyholder and underlying investments.

The Pitfalls of Overseas Insurance Policies: How Foreign Insurance Can Trigger Tax Issues

Foreign-issued life insurance policies can pose serious tax risks for U.S. taxpayers. Many policies sold overseas do not meet the U.S. definition of “life insurance” under the Internal Revenue Code and are instead treated as foreign investment accounts.

In practice, many immigrant families who purchased insurance abroad discover that their policies generate taxable income annually. In some cases, they may also face excise taxes and significant reporting penalties.

For individuals living in or moving to the United States, ensuring that their insurance policies meet U.S. tax standards is critical. Our experience shows that most foreign-issued policies fail to qualify as U.S.-compliant life insurance, triggering U.S. income tax, excise tax, and foreign asset reporting obligations such as FBAR.

Moreover, foreign insurance products with cash value components may fall under FATCA reporting requirements. Insurers issuing such products are often classified as Foreign Financial Institutions (FFIs) and must report U.S. account holders to tax authorities.

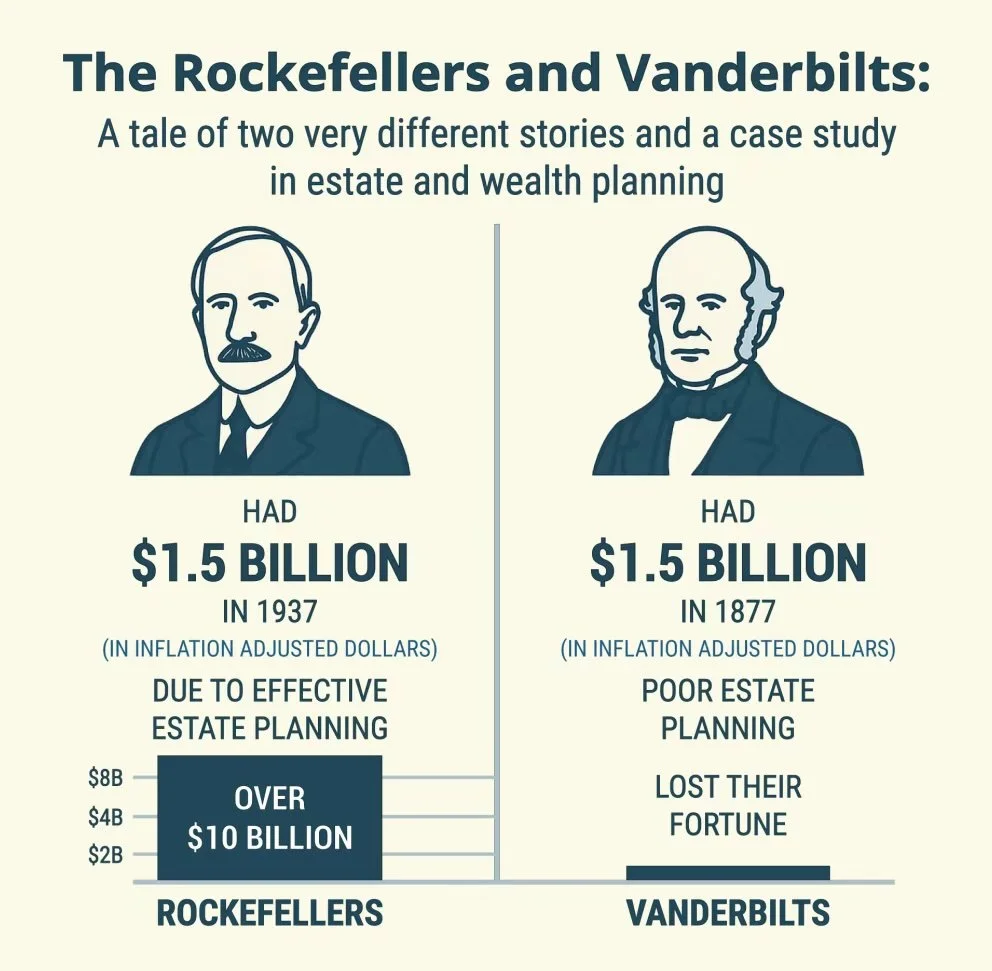

Lessons from History: A Comparison Between the Rockefeller and Vanderbilt Families

History offers a powerful comparison. In the late 19th century, both the Rockefeller and Vanderbilt families were among the wealthiest in America. Today, the Rockefeller family’s wealth has endured for generations, largely due to disciplined use of trusts and insurance structures. In contrast, the Vanderbilt fortune largely dissipated within a few generations.

For today’s ultra-wealthy families, life insurance—especially when integrated with trust planning—can determine whether wealth disappears or endures across generations.